Updated June 2026

What Is Liability Insurance Insurance?

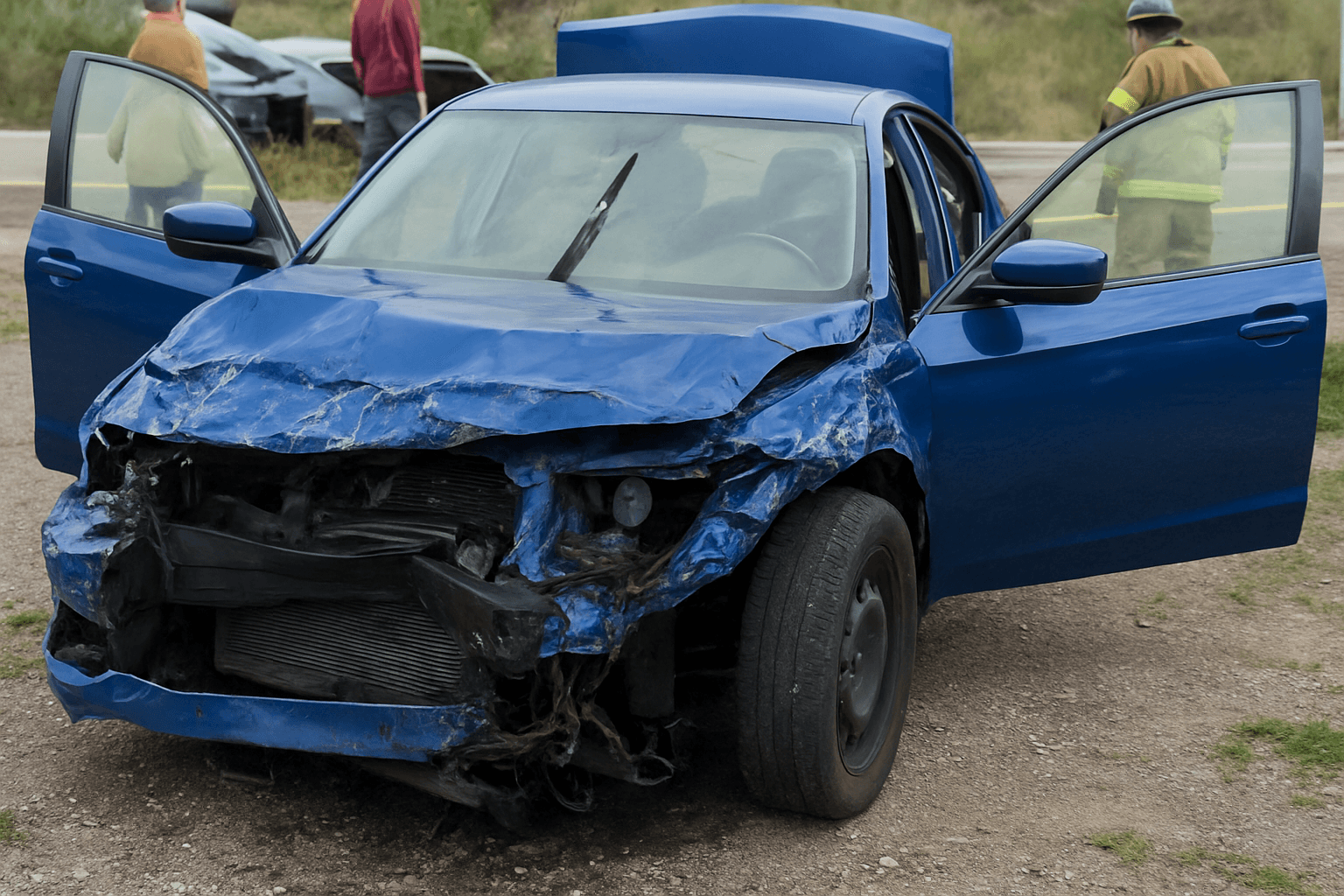

Liability insurance is split into two parts: bodily injury liability, which pays medical expenses, lost wages, and legal costs when you injure someone in an accident, and property damage liability, which covers repair or replacement of other people's vehicles and property you damage. Colorado requires 25/50/15 minimums — $25,000 per person for injuries, $50,000 per accident for total injuries, and $15,000 for property damage. If you cause an accident and the damages exceed your liability limits, you are personally responsible for the difference, which can result in wage garnishment or asset seizure.

- You rear-end a stopped car at a red light. The other driver has $18,000 in medical bills and $6,500 in vehicle damage. Your 25/50/15 liability policy pays the full $18,000 in medical costs and the full $6,500 for vehicle repairs. Your own car's $4,200 in front-end damage is not covered — you pay out of pocket or file a collision claim if you carry that coverage.

- You cause a three-car accident. Two injured parties have combined medical bills of $78,000. Your liability policy pays the $50,000 per-accident bodily injury limit, but you are personally liable for the remaining $28,000. The injured parties can sue you for the shortfall, and Colorado courts can order wage garnishment to satisfy the judgment. This is why suspended license drivers reinstating with SR-22 often purchase higher liability limits than the state minimum.

- You slide through an intersection and total a parked luxury SUV valued at $62,000. Your $15,000 property damage liability limit pays only $15,000. The vehicle owner's insurance company pays the remaining $47,000 to their policyholder, then subrogates against you — meaning they will pursue you in court for reimbursement. Colorado does not cap subrogation claims, and the debt does not discharge until paid or settled.

Who Needs Liability Insurance Insurance?

You need liability insurance in Colorado if you own a registered vehicle, even during a license suspension — driving or not, registration requires proof of continuous coverage. SR-22 filers must maintain liability coverage for the entire three-year filing period without a single-day lapse, or the state re-suspends your license and restarts the clock. If you do not own a vehicle but need SR-22 to reinstate, a non-owner liability policy satisfies Colorado's requirement and costs 30–50% less than standard policies.

If you own a car or need SR-22, liability insurance is mandatory — no decision to make. If you are suspended without SR-22 requirement and do not own a vehicle, you can skip coverage until reinstatement. If you drive occasionally using a borrowed car, consider non-owner liability to protect yourself from personal financial liability in an at-fault accident, even if the state does not require it. Non-owner policies cost $30–$70 per month and cover you in any vehicle you drive with permission.

How Much Does Liability Insurance Insurance Cost?

Liability-only coverage in Colorado costs approximately $45–$95 per month for state minimum 25/50/15 limits, or $540–$1,140 annually. SR-22 filers with suspended license history typically pay $75–$160 per month due to high-risk classification, even for minimum liability limits.

- Driving record — DUI convictions, at-fault accidents, and excessive points violations increase liability premiums by 60–180% in Colorado for the first three years after the incident.

- SR-22 filing requirement — adding SR-22 to a liability policy adds $15–$35 per month in filing fees and high-risk surcharges, separate from the base liability premium.

- Coverage limits selected — increasing from Colorado's 25/50/15 minimum to 100/300/100 typically adds $20–$50 per month, but reduces personal financial exposure in serious accidents.

- Zip code and county — Denver, Aurora, and Colorado Springs drivers pay 25–40% more for liability coverage than rural county residents due to higher accident frequency and claim severity.

- Age and experience — drivers under 25 or over 70 pay higher liability rates, and newly licensed drivers of any age face surcharges until they establish a three-year clean driving record.

- Lapse history — any gap in liability coverage longer than 30 days in the past 12 months increases premiums by 15–35%, and SR-22 filers who lapse restart their full three-year filing period.